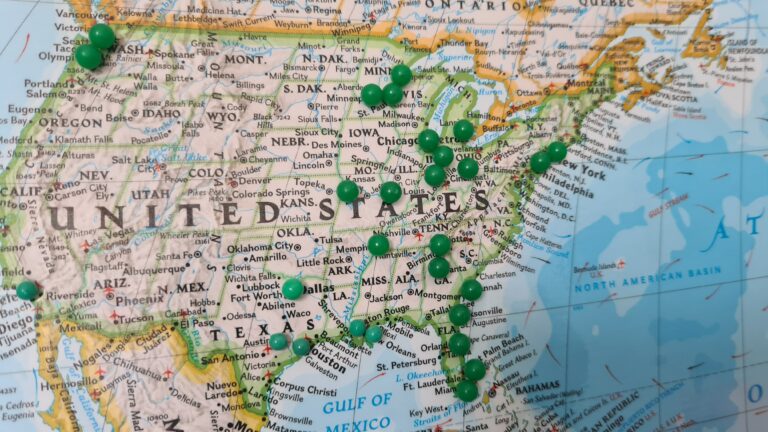

Is Estate Planning Affected by Property in Two States?

Cleveland Jewish News’ recent article titled “Use attorney when considering multi-state estate plan” says that if a person owns real estate or other tangible property (like a boat) in another state, they should think about creating a trust that can hold all their real estate. You don’t need one for each state. You can assign or deed their property to the trust, no matter where the property is located.

Some inherited assets require taxes be paid by the inheritors. Those taxes are determined by the laws of the state in which the asset is located.

A big mistake that people frequently make is not creating a trust. When a person fails to do this, their assets will go to probate. Some other common errors include improperly titling the property in their trust or failing to fund the trust. When those things occur, ancillary probate is required. This means a probate estate needs to be opened in the other state. As a result, there may be two probate estates going on in two different states, which can mean twice the work and expense, as well as twice the stress.

Having two estates going through probate simultaneously in two different states can delay the time it takes to close the probate estate.

There are some other options besides using a trust to avoid filing an ancillary estate. Most states let an estate holder file a “transfer on death affidavit,” also known as a “transfer on death deed” or “beneficiary deed” when the asset is real estate. This permits property to go directly to a beneficiary without needing to go through probate.

A real estate owner may also avoid probate by appointing a co-owner with survivorship rights on the deed. Do not attempt this without consulting an attorney.

If you have real estate, like a second home, in another state (and) you die owning that individually, you’re going to have to probate that in the state where it’s located. It is usually best to avoid probate in multiple jurisdictions, and also to avoid probate altogether.

A co-owner with survivorship is an option for avoiding probate. If there’s no surviving spouse, or after the first one dies, you could transfer the estate to their revocable trust.

Each state has different requirements. If you’re going to move to another state or have property in another state, you should consult with a local estate planning attorney.

Reference: Cleveland Jewish News (March 21, 2022) “Use attorney when considering multi-state estate plan