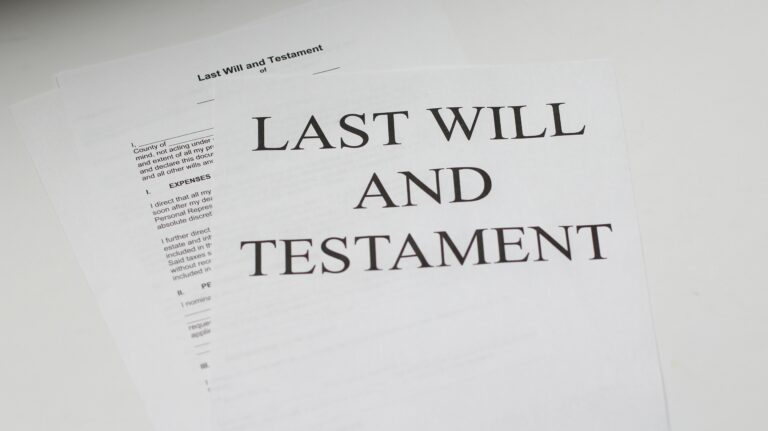

What Assets are Not Considered Part of an Estate?

In presentations regarding essential actions individuals should take regarding inheritance, emphasis is usually placed on drafting a will. This leaves unanswered what happens to assets that do not pass by will —so called non-probate assets.